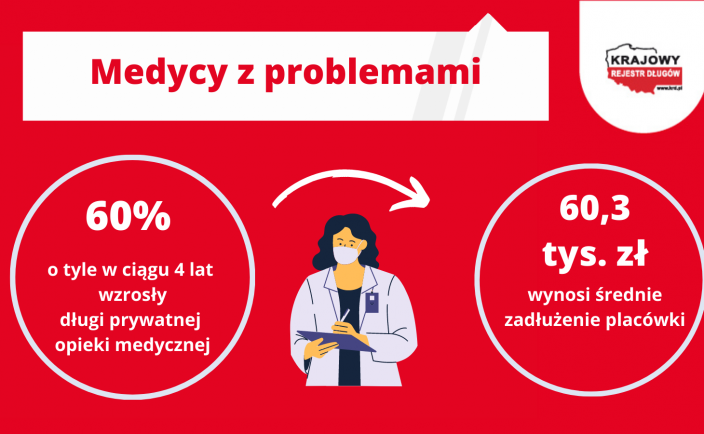

- Lendtech

- 28.04.2023

The next edition of the FinTech&InsurTech Digital Congress will be held on 17th – 18th May 2023. One of the event’s highlights will be a debate on the Great Market Purge. In the article, we present some facts about this phenomenon. Click the link https://fintechdigitalcongress.pl/lp/lpm/en/ to register for the event and read the agenda.

Here is a recap of the article:

- Great market purge is a term used to describe the phenomenon of survival of those companies that have managed to adapt to the changing market situation.

- Investors focus on companies that use technological innovation and apply ESG, among other things.

- The deceleration of start-ups’ financing is due to limited capital, among other factors. In such a situation, networking, diversifying sources of funding, investing in innovation and adapting to a rapidly changing market may be the solution.

- The development of the FinTech industry is driven by technological advances, changes in consumer behaviour, regulation, globalization and innovation.

The changing economic climate and the phenomenon of „The Great Market Purge”

Rising inflation, the changing economic climate and the ongoing Russian-Ukrainian war have a far-reaching impact on the companies. „The Great Market Purge” is an informal term that refers to the process of elimination or consolidation of weaker players in an industry. This phenomenon results from increasing competition, changing regulations and technological advances, which means that only the strongest and most innovative companies survive the crisis. Interestingly, this phenomenon repeats itself in cycles.

The current economic instability makes it necessary for companies to react dynamically to changing market conditions if they want to stay afloat. That means that the companies should:

- look for opportunities to reduce expenses because of the rising operating costs and customers’ pressure for better financial and insurance terms due to rising inflation;

- seek alternative sources of financing because of less access to capital due to changes in investors’ behaviour;

- effectively manage currency risk;

- be flexible and quick in adaptation to changing regulations.

Additionally, the financial and insurance companies need to:

- monitor increasing customer credit risk and apply appropriate strategies to manage it;

- adjust risk assessment models because of changes in the prices of insurance policies;

- adjust their offerings to meet the customers’ expectations of the products that protect against inflation;

- adjust their expansion strategies to foreign markets, considering political and financial risks.

What is the state of investments in the digital economy?

Investments in the digital economy are primarily based on new technologies that transform traditional economic sectors and create new business models. Investors are looking for companies that can leverage technological innovations to streamline business processes, increase efficiency, improve service quality and create new market opportunities. As the digital economy continues to grow, investors will seek to identify and then support companies that have the potential to become leaders in their sectors.

In addition, investors are increasingly paying attention to social and environmental responsibility (ESG) when making investment decisions. Therefore, companies that demonstrate a commitment to sustainability, care about the well-being of employees and adhere to business ethics are likely to attract more attention from investors.

Considering the development of investments in the digital economy, it is necessary to emphasize how important it is to skillfully diversify the sources of investments, such as venture capital (VC) funds, private equity (PE) funds, corporations, angel investors or individual investors, among others. Each has its strategies, goals and investment criteria that influence the choice of investments and how to support the growth of a company’s investment portfolio.

It must not be forgotten that investments in the digital economy carry risks. Therefore, investors should carefully evaluate them and use appropriate strategies to manage them, such as diversifying their portfolios or investing at different stages of development.

The situation of start-ups in a challenging economic environment. What factors hinder funding, and how to deal with them?

Factors contributing to the inhibition of start-ups financing in Poland include limited access to capital, lack of investor experience, low levels of international cooperation, regulations and bureaucracy, and entrepreneurial culture.

Start-ups, to overcome these challenges, are advised to build strong networks, participate in accelerator programs and incubators, diversify funding sources, collaborate with other companies, invest in developing team competencies, promote their business, and maintain flexibility and adaptability.

In the developed digital economy, startups can increase business opportunities by applying innovation, introducing novel products and services, leveraging cutting-edge technologies such as artificial intelligence or blockchain, focusing on User Experience by offering superior experiences, scaling the business and pursuing easily scalable solutions, partnering with other companies or participating in accelerator programs. Additionally, a start-up must be able to adapt quickly to the requirements of a rapidly changing digital world, attract and retain talents, diversify funding sources and make headway in international markets. These activities increase a startup’s competitiveness and attractiveness to investors and customers.

What is driving the growth of the Fintech industry?

The development of the Fintech industry is driven by technological and market factors contributing to the transformation of the financial sector. These include technological advances that enable new products and services, the widespread use of the Internet and mobile devices (increasing demand for financial applications), changing consumers behaviours who expect convenient and fast solutions, regulations that favour FinTech development, globalization, the scarcity of financial services, competition and innovation, investment support, partnerships and collaborations, and the development of technological infrastructure.

Technological innovations such as artificial intelligence, machine learning, blockchain and IoT streamline business processes. Fintech companies offer international transfers, foreign currency transactions and banking services to people with different residency statuses. They fill gaps in financial services by providing microloans, micro-investments and savings accounts. Competition and innovation force traditional financial institutions to adapt, accelerating Fintech development. The growing interest in innovation attracts investments from venture capital funds, corporations and individual investors. Collaboration between Fintechs and traditional financial institutions becomes more common, contributing to the growth of innovation. The increased availability of cloud computing, network bandwidth and computing resources enables Fintechs to deploy and scale their solutions rapidly.

Autor: Lendtech | Data publikacji: 28.04.2023

![Polacy w obliczu inflacji sięgają po oszczędności [BADANIE]](https://www.lendtech.pl/wp-content/uploads/2022/08/josh-appel-netpasr-bmq-unsplash_md-704x434.jpg)

![Xelo Pay, czyli fintech płatniczy bez haczyków [Wywiad]](https://www.lendtech.pl/wp-content/uploads/2022/02/Xelo-Pay-czyli-fintech-platniczy-bez-haczyków-Wywiad--704x434.webp)

![O ile wzrosną raty kredytu hipotecznego po podwyżce stóp procentowych? [KALKULATOR]](https://www.lendtech.pl/wp-content/uploads/2022/02/O-ile-wzrosną-raty-kredytu-hipotecznego-po-podwyżce-stóp-procentowych-KALKULATOR--704x434.webp)